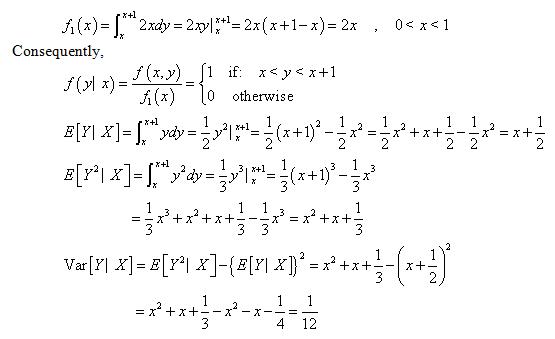

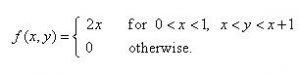

The stock prices of two companies at the end of any given year are modeled with random variables X and Y that follow a distribution with joint density function

What is the conditional variance of Y given that X = x ?

- 1/12 Correct Answer

- 7/6

- x + 1/2

- x2 – 1/6

- x2 + x + 1/3

Solution: A

Let f1(x) denote the marginal density function of X. Then