An insurance policy pays for a random loss X subject to a deductible of C, where 0 < C < 1. The loss amount is modeled as a continuous random variable with density function

Given a random loss X, the probability that the insurance payment is less than 0.5 is equal to 0.64 .

Calculate C.

- 0.1

- 0.3 Correct Answer

- 0.4

- 0.6

- 0.8

SOLUTION: B

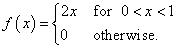

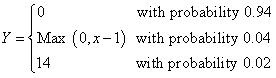

Denote the insurance payment by the random variable Y. Then

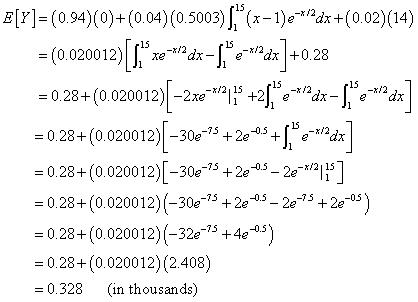

and

It follows that the expected claim payment is 328.